Silicon Valley Bank and Banking Theology

Why the American Banking System's "Held to Maturity" and "Available for Sale" Asset Classifications Matter

Much has been written, and will be written, about the collapse of Silicon Valley Bank (SVB.) The definitive account of how a bank with more than $200 billion in assets vaporized almost overnight will take time to construct. This is a short exploration of the asset classification system that is one part of the theology, or belief system, of American banking and how it relates to SVB’s failure.

A Bank’s Choice: Are Assets “Held to Maturity” or “Available for Sale”?

The most detailed news accounts of SVB’s collapse describe an asset classification choice that banks are permitted to make to comply with regulatory requirements designed to insure they have sufficient capital. Banks are permitted to designate investments (acquired with deposits and other assets) as “held to maturity” (HTM), meaning that the bank intends to hold the investment, often a bond or other security issued by the Department of the Treasury, until its due date when the principal and accrued interest will be paid to the investing bank.

The advantage of designating assets as HTM is that the bank can carry the assets on its books at their amortized cost, or essentially the price paid for the asset. If interest rates on, say, Treasury bonds, rise above the interest paid on the HTM assets the market value of those bonds declines. However, because those assets are designated HTM, the bank is not required to realize a loss—the HTM assets continue to be carried on the bank’s books for regulatory capital compliance purposes at their amortized cost.

One argument for the HTM designation of assets is that if a bond really is held to maturity interim price movements should not matter: the principal and interest on the bond accurately represents the bank’s capital. Another argument supporting HTM classification is that when interest rates rise, the rates banks pay on deposits do not rise point for point. In other words, the spread widens between what the bank earns on its assets and what the bank is obliged to pay depositors. This makes the deposits more valuable to the bank just as its HTM-designated bonds become less valuable, provided the deposits stay in the bank. If the deposits stay in the bank, everything works out fine in the long run.

A detailed March 14 story, Inside the Collapse of Silicon Valley Bank, in The New York Times shows that SVB relied extensively on HTM asset classification. The Times reported:

As of Dec. 31, SVB classified most of its debt portfolio, or roughly $95 billion, as “held to maturity.” Because of an accounting loophole, the bank didn’t have to show fluctuations in the value of those bonds on its balance sheet.

On average, banks with at least $1 billion in assets classified only 6 percent of their debt in this category [HTM] at the end [of] 2022. But Silicon Valley Bank put 75 percent of its debt as held to maturity, according to a research report by Janney Montgomery Scott.

The complete story can be read

The HTM classification is subject to an important condition: if the bank sells any of its HTM assets then, all of its HTM assets are automatically designated as “available for sale,” meaning that such assets must be carried on the bank’s books at their market value—the assets are “marked to market.”

Should the high percentage (relative to other banks) of SVB’s assets classified as HTM have been a bigger warning signal to the bank’s regulators? Stay tuned for investigations, reports and statements by politicians on this issue.

Large U.S. Banks Extensively Reclassified Assets as HTM in 2022

SVB classified Treasury bonds as HTM when it acquired them—effectively betting that interest rates would go down. On March 30, the Journal reported that it had identified six large U.S. banks that together reclassified more than $500 billion in previously acquired bond holdings in 2022. The Journal reported:

The banks’ held-to-maturity bonds had a combined $1.14 trillion balance-sheet value as of Dec. 31, up from $681 billion a year earlier. The increase was mainly due to the reclassifications.

The $1.14 trillion figure was $118 billion, or 12%, higher than the bonds’ fair market values, disclosed in footnotes to the banks’ financial statements. The $118 billion was equivalent to 18% of the banks’ total equity, which is the difference between assets and liabilities.

The complete article can be read

Thus, HTM reclassification by the large banks had a significant effect on making their balance sheets look better than they would have if their HTM-designated assets had been reported at fair market value.

Does the “Held to Maturity” Versus “Available for Sale” Asset Classification Distinction Make Sense?

Treasury-issued debt securities are subject to complete price discovery—the market price of a Treasury bond is ascertainable on a computer screen in second-by-second intervals. Thus, there would seem to be a more accurate picture of a bank’s capital position if all its assets were deemed “available for sale” and booked at their market value. In other words, is there any real purpose to the HTM classification?

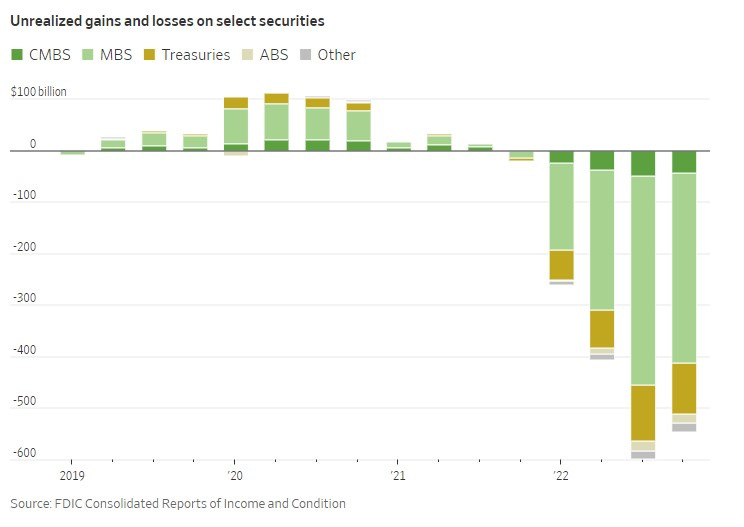

The question seems logical. However, SVB’s collapse, and the way the banks have managed risk as interest rates increased, suggest that eliminating HTM classification may further stress the banking system. An article in The Wall Street Journal’s March 25-26 edition, The Economy Changed, Bank Regulation Didn’t reports that the aggregate unrealized losses on securities held by U.S. banks now exceed $500 billion, or roughly twice the size of SVB’s asset base at its peak.

These unrealized losses are not due solely to the classification of assets as HTM. A Journal chart illustrates that the banks’ unrealized losses derive mainly from holdings in four types of securities. The largest portion of the unrealized losses is attributable to mortgage-backed securities (MBS). There are also unrealized losses in bank holdings of commercial mortgage-backed securities (CMBS), asset-backed securities (ABS) and United States Treasury obligations (“Treasuries.”)

The complete article can be seen

Journal opinion writers suggest that HTM classification helped to hide SVB’s true financial condition and advocate for banking system change. A column in the March 29 edition said that, “[B]y December 2022, SVB had an unrecognized loss of $24 billion on its hold-to-maturity securities combined with a new reliance on hot money.” The column asserts:

Instead of raising the deposit insurance limit or expanding supervisor powers, Congress should require all assets held by banks to be marked to market.

The column can be read

The marking of all bank assets to market—the elimination of the HTM classification— would be a significant revision to American banking theology. In the near term, at least, bank balance sheets would look significantly worse. Would the additional transparency derived from marking all bank assets to market be worth the shock to the banking system?

Possible Takeaways

SVB was not the only bank that has miscalculated risk as interest rates increased. The reclassification of assets as HTM by large banks in 2022 now looks like the “go to” move to preserve balance sheet appearances when, in fact, there were significant declines in total equity. The accounting consequence of HTM classification seems to outweigh the reasons—the theology—supporting it. The problem for policy makers is that eliminating the HTM classification of assets in the worthy pursuit of accurate financial reporting by banks would further stress the banking system.

Banking, as some wise guy said, is a confidence game.1

Your comments are very welcome.

In some respects, banking is an upside-down world. Many people would consider a debt owed to them by someone else to be a problem because of the nonpayment risk. Banks record their loans—debts owed to them—as balance sheet assets. The banking environment is changing. The universe of those who can and will move large amounts of money at a click seems to be expanding. Big money transfers have mostly been the province of financial professionals. SVB’s collapse shows that this capability can now exercised by depositors who can communicate with each other instantaneously and continuously. So, assumptions about the stability of deposits—or deposit “stickiness”—may need revisiting. Almost every account of what happened at SVB focuses on the rapidity—$42 billion in one day—of the deposit flight. Money, and information about money, now move with unprecedented velocity. Let’s hope that bank regulators closely examine what happened at SVB and develop systems to address this need for speed.

I can only hope this is the last banking crisis of my lifetime. However, because that wish may not come true, it’s good to know about Available for Sale versus Held-to-Maturity, and why the distinction matters.