Down in the Weeds at Potomac Yard

Monumental Sports and Entertainment's Description of the Risks of the Potomac Yard Project to Alexandria and Virginia

A large crowd attended the City Council’s January 27 town hall at the Charles Houston Recreation Center about the proposed sports and entertainment complex at Potomac Yard.

What follows uses public information to clarify communications from one of the project’s proponents, Monumental Sports and Entertainment (MSE), about the potential economic risks of the project to Alexandria and Virginia.

Now Available: Multiple Information Sources

There is abundant information from a variety of sources about the proposed sports and entertainment complex at Potomac Yard. At the town hall, several City Council members emphasized the importance of the public’s receipt of accurate and complete information about the project.

MSE and the Alexandria Economic Development Partnership have created websites that describe various aspects of the project and its projected benefits. AEDP’s website is

and MSE’s is

Representatives of the Coalition to Stop the Arena were also present before and at the town hall.

The coalition’s website is

Down in the Weeds About the Potomac Yard Project’s Potential Transaction Risks

MSE’s website features a Fact Check section that addresses myths and possible misimpressions about the Potomac Yard project. Here is how MSE’s Fact Check section dispels one of the myths about the project:

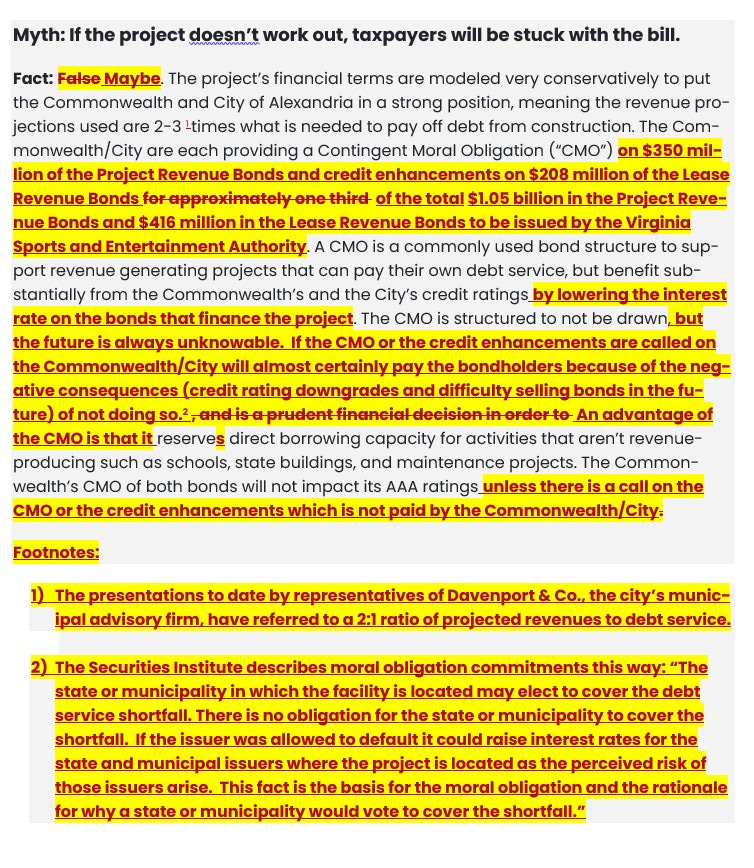

MSE’s explanation could be more informative. Here is a revised version of MSE’s fact check that contains edits and footnotes based on public information.

MSE’s fact check, 1) does not describe the size ($558 million each) of the contingent payment obligations incurred by the city and the commonwealth, 2) does not quantify the total debt—the Project Revenue Bonds ($1.05 billion) plus the Lease Revenue Bonds ($416 million)—to be issued by the Virginia Sports and Entertainment Authority (VSEA), 3) does not describe how the city and commonwealth’s contingent moral obligations work, and 4) does not disclose that a contingent moral obligation, though not legally enforceable, is binding as a practical matter because of the negative consequences to a city or state of not honoring such an obligation.

Possible Takeaways

Here are possible fact-based conclusions about the Potomac Yard project’s transaction risks to Alexandria and the commonwealth.

1. The Project’s Financial Risks to Alexandria and Virginia Can be Calculated. The contingent payment obligations incurred by the city and the commonwealth in the Potomac Yard transaction are quantifiable. Each incurs a $350 million moral obligation on the Project Revenue Bonds and $208 million in credit enhancements on the Lease Revenue Bonds. MSE’s fact check describes economic risk without quantifying it, thus telling only part of the story for anyone seeking to understand the transaction.

2. As a Practical Matter, Alexandria and Virginia Will Each Guarantee $558 Million of the Potomac Yard Project’s Bonds. The contingent moral obligation ($350 million each for the city and the commonwealth on the Project Revenue Bonds) is not an enforceable legal obligation. A failure to pay the contingent moral obligation, or the credit enhancements of $208 million each for the city and the commonwealth on the Lease Revenue Bonds, would impair the city and commonwealth’s credit ratings and access to the debt markets. As a practical matter, this makes the city and the commonwealth’s contingent moral obligations enforceable guarantees.

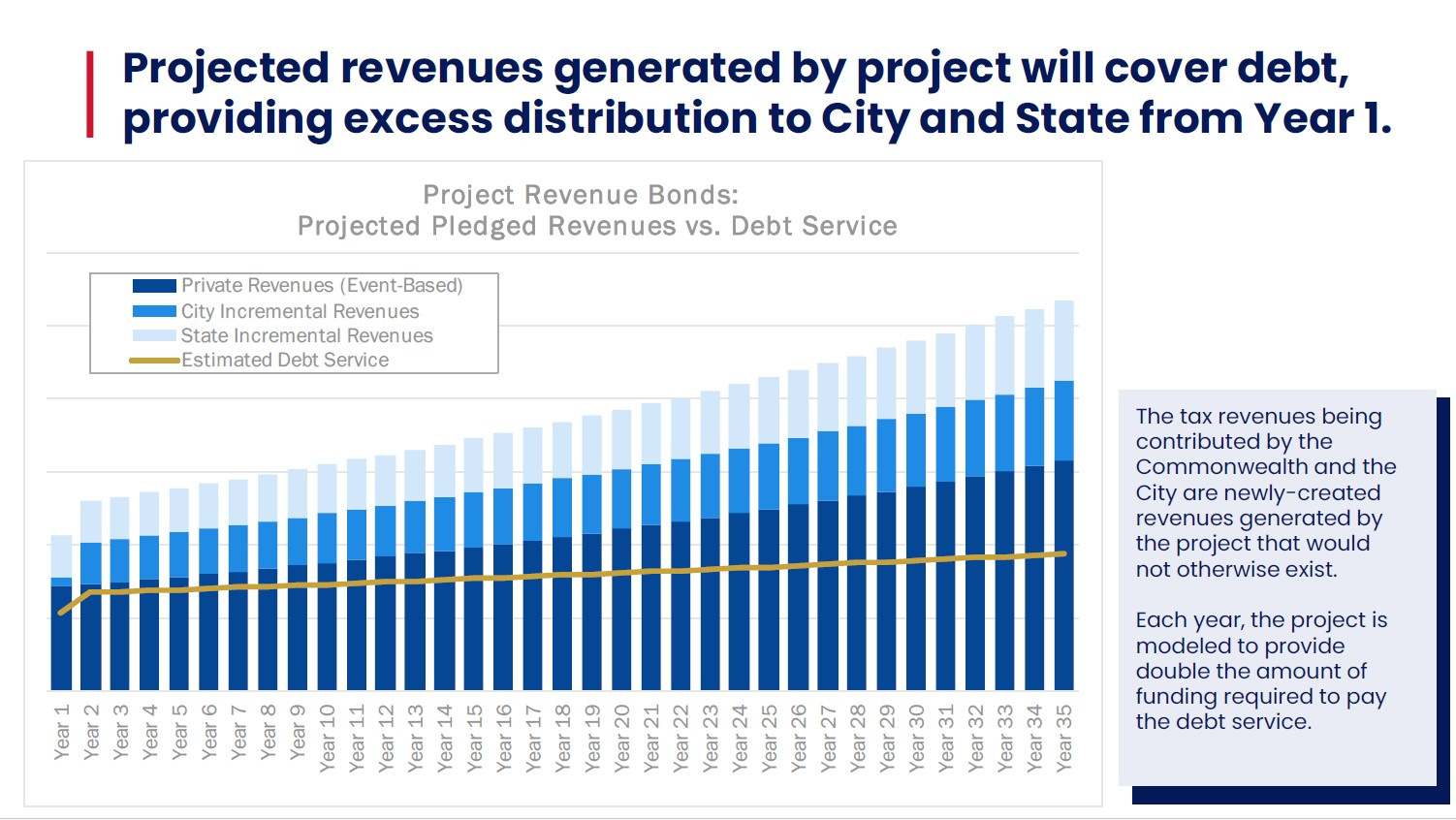

3. Related and Essential: The Absence of a Bond Default and the Revenue and Debt Service Projections. For the city and the commonwealth, the Potomac Yard transaction is premised on the non-occurrence of an event, namely, a default on VSEA’s bonds. Accordingly, the revenue and debt service projections for the project are critically important: they show how the city and the commonwealth will be insulated by anticipated revenues from the consequences of a default.

The revenue and debt service projections were presented at the City Council’s January 23 meeting and at the January 27 town hall. Here they are:

The projections are presented in an aesthetically appealing graphic. While attractive as an artwork, the illustrated projections lack a y-axis, or vertical number line, that shows the dollar amounts represented by the revenue bars and debt service line.

Enough nitpicking: the real issues, of course, are the validity of the assumptions and methods that support the projections. These are topics for another time.

Your comments are very welcome.

Thank you for this information. It is hard for me to take a meaningful position without the fiscal facts. Most especially there is a lack of detailed Revenue and Debt Service Projections as you point out. The PR outreaches are a waste of time without the data.

I suspect the JP Morgan report (cited in the Washington Post and closely held by the governor’s office) may have a more complete assessment of the risks to the lenders. In my experience, lenders model project financing to aim at a 2x debt coverage, which is seldom realized. Sensitivity model runs with alternative revenue projections tied to key revenue drivers will have tested the downside for the banks. The city and commonwealth $1.1 billion backstop to protect the bond holders must be a result of JP Morgan’s analysis of the risks. It would be a clear public service for our representatives to release that report and not just the flimsy stuff they’re now showing us.

Leonard Crook